It’s not just your imagination if your paycheck in 2026 looks a little bigger than it did last year. The federal government’s choice to lower the lowest tax rate to 14 percent, along with inflation adjustments for all brackets, means that most Canadians will keep more of their money. At first glance, the changes may not seem like much, but knowing how they affect marginal tax rates and other planning strategies can have a big effect on your finances.

In this guide, we’ll explain how Canada’s progressive tax system works, break down the 2026 federal tax brackets, and give you steps you can take to lower your tax bill.

What Were the Changes in Federal Taxes in 2026

The most talked-about change for 2026 is that the lowest federal income tax rate will go from 15% to 14%. This cut first happened in the middle of 2026, which means that taxpayers last year paid a rate of about 14.5 percent. The lower rate will be in effect for the whole year in 2026, so Canadians will be able to fully benefit from it.

Canada Tourism Outlook for 2026: Visitor Growth Continues but U.S. Travel Decline Raises Concerns

Canada Tourism Outlook for 2026: Visitor Growth Continues but U.S. Travel Decline Raises Concerns

In addition to this big change, the Canada Revenue Agency (CRA) has raised the limits on all five federal tax brackets to keep up with inflation. This stops “bracket creep,” which is when inflation pushes people into higher tax brackets even though their real buying power hasn’t changed.

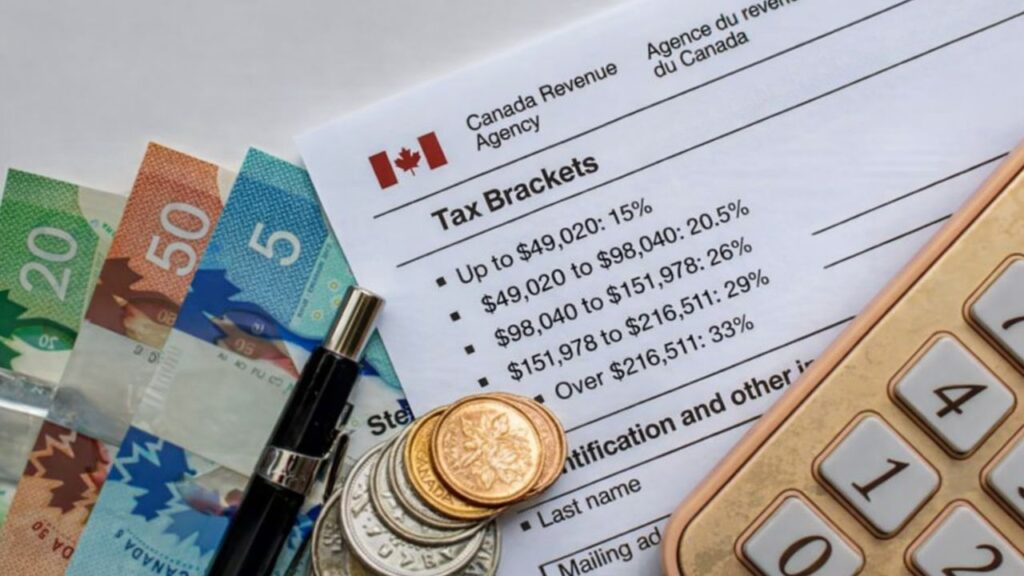

This is how the federal tax brackets will look in 2026:

- 14% on the first $58,523 of taxable income (down from 15% on $57,375)

- 20.5% on income between $58,523 and $117,045 (previously $57,375 and $114,750)

- 26% on income between $117,045 and $181,440 (previously $114,750 and $177,882)

- 29% on income between $181,440 and $258,482 (previously $177,882 and $253,414)

- 33% on income over $258,482 (before it was $253,414)

The Department of Finance Canada says that this cut will save Canadians more than $27 billion in taxes over the next five years. The effect is smaller for individual households, but it’s still important, especially for those with the lowest incomes who will benefit the most directly.

“Canada Tax Brackets 2026: What’s Different and How to Pay Less in Taxes”

What You Need to Know About Marginal Tax Rates in Canada

A common mistake people make when it comes to personal finance is thinking that if you make enough money to move up to a higher tax bracket, all of your income will be taxed at the higher rate. This is not the case.

Canada has a progressive tax system, which means that different parts of your income are taxed at different rates. Only the money that falls within a certain range is taxed at that range’s rate.

If you make $70,000 in 2026, for instance:

- The first $58,523 is taxed at a rate of 14%.

- The other $11,477 is taxed at 20.5%.

Your overall effective tax rate is much lower than 20.5%, which shows that moving up to a higher tax bracket doesn’t mean you lose more money overall.

Why Marginal Rates Are Important for Your Paycheck

Knowing about marginal tax rates can help you avoid worrying about money that isn’t necessary. A lot of people don’t want to take a raise or bonus because they think they will be “punished” with higher taxes. In reality, your total take-home pay always goes up, even if a raise puts you in a higher tax bracket. The only difference is that some benefits that are based on income, like some credits or government support programs, may go down as income goes up.

Smart Ways to Lower Your 2026 Tax Bill

You can still improve your tax situation even with lower brackets and adjustments for inflation. Here are some real ways to make a difference:

Put more money into your RRSP

One of the best ways to lower your taxable income is still to use a Registered Retirement Savings Plan (RRSP). Contributions lower the amount of money you have to pay taxes on, and the investments grow without being taxed until you take them out, which is usually when you retire when your tax rate may be lower.

The RRSP contribution limit has gone up to $33,810 for 2026, up from $32,490 in 2025. Your personal limit is the smaller of 18% of your earned income from the previous year or the annual cap, plus any unused contribution room that you have left over. You can check your available limit on CRA My Account.

If you missed the RRSP deadline for the 2025 tax year (March 2, 2026), you can still lower your taxable income by the end of the year by planning your 2026 contributions early. Putting money into an RRSP on a regular basis is a long-term plan that saves you more and more money on taxes over time.

Take Advantage of Every Credit and Deduction You Can

A lot of Canadians don’t claim all of the deductions and credits they can, which means they lose money. There are a few changes for tax season 2026, such as new credits and new due dates for existing ones.

Some common deductions and credits are:

- Childcare costs: You may be able to deduct the costs of daycare, preschool, or after-school programs.

- Moving costs for work: If you move for a job, some of the costs can lower your taxable income.

- Home office deduction: Employees who work from home can still claim expenses for their workspace after the pandemic.

- Medical costs: Only the part that is above a certain amount counts, but big costs can lead to big deductions.

- Credits for tuition and education: You can claim amounts that you didn’t use in previous years because of carry-forward rules.

The most important thing is to keep detailed records and check eligibility twice. If you miss even one deduction, you could be leaving hundreds of dollars on the table.

Share your income with your spouse or partner.

If one partner makes a lot more money than the other, income splitting can help lower the amount of taxes your household has to pay.

- The higher-income spouse puts money into an RRSP in the name of the lower-income spouse. This lets the contributor take the deduction, and the recipient’s lower marginal rate will apply to the withdrawals later on.

- Pension income splitting: Retirees can give up to 50% of their eligible pension income to their spouse or common-law partner. This effectively moves money from a higher tax bracket to a lower one, which lowers the total amount of taxes owed.

Income splitting works best when there is a big difference between the incomes of the two spouses or when you are planning for tax savings in retirement.

How changes in inflation affect your taxes

The changes to the 2026 brackets may seem small, but they help Canadians avoid paying more taxes just because prices go up. For example, if wages go up by 2% without indexing, a taxpayer could move up to a higher bracket even though their real purchasing power hasn’t changed.

Every year, the CRA adds an indexation factor to all federal brackets to stop bracket creep. This makes sure that Canadians get nominal wage increases without being unfairly taxed on gains that come from inflation.

How to Get the Most Out of Your Paycheck

Canadians can do more than just put money into their RRSPs and claim deductions to lower their tax bills:

- Timing your income and expenses: If it keeps you in a lower tax bracket, you might want to wait until a later year to get your bonuses or income. If you think your taxes will be higher next year, you should also speed up deductible expenses into this year.

- Use Tax-Free Savings Accounts (TFSA): Money you put into a TFSA doesn’t lower your taxable income, but it does grow tax-free and you can take it out without paying taxes. By combining TFSA and RRSP contributions, you can plan your taxes more flexibly.

- Use professional advice: A qualified accountant or financial planner can help you find credits, deductions, and ways to split your income that you might not have thought of.

You can have more control over your money and pay less in taxes by making even small changes.

Understanding the Bigger Picture of the Tax Changes in 2026

The 2026 tax changes aren’t ground-breaking, but they do show a bigger trend toward small tax breaks for Canadians. The lower bottom bracket and inflation-adjusted thresholds together have a big effect, especially on families with moderate incomes.

These changes also show how important it is to plan ahead for taxes. If you wait until tax season to make the most of your situation, you won’t be able to save as much money on taxes. Making early contributions to RRSPs, keeping careful track of deductions, and coming up with smart ways to split income can all make a big difference.

A Note About Planning for the Long Term

Taxes are only one part of a bigger plan for your money. Including RRSPs, TFSAs, and ways to split your income into your long-term plan can make you more ready for retirement, help your cash flow, and lower your stress. Even small annual tax savings add up over time, giving you more money to invest, pay off debt, or reach big life goals.

In conclusion, how to make the most of your 2026 paycheck

There aren’t any big changes to the federal tax year in 2026; instead, there are small changes that help Canadians manage their money better. You can get the most out of these changes by learning about marginal rates, using RRSP contributions, claiming all available credits, and looking into ways to split your income.

It might not seem like much of a difference from month to month, but with careful planning, you can keep more of your hard-earned money over the course of a year. In 2026, you can make your paycheck go further by paying attention to your income, deductions, and timing. You can also set yourself up for long-term financial health.